SIMPLE (SAVINGS INCENTIVE MATCH PLAN FOR EMPLOYEES) IRA

Employees elect salary deferrals to fund their SIMPLE IRA and receive matching contributions from their employer. Employer matches can be either 3% of the employee’s contribution or 2% of the employee’s annual compensation. In 2020, employees can defer up to $13,500 of their salary, pretax, and those who are 50 or older can defer up to $16,500 by taking advantage of a $3,000 catch-up contribution.

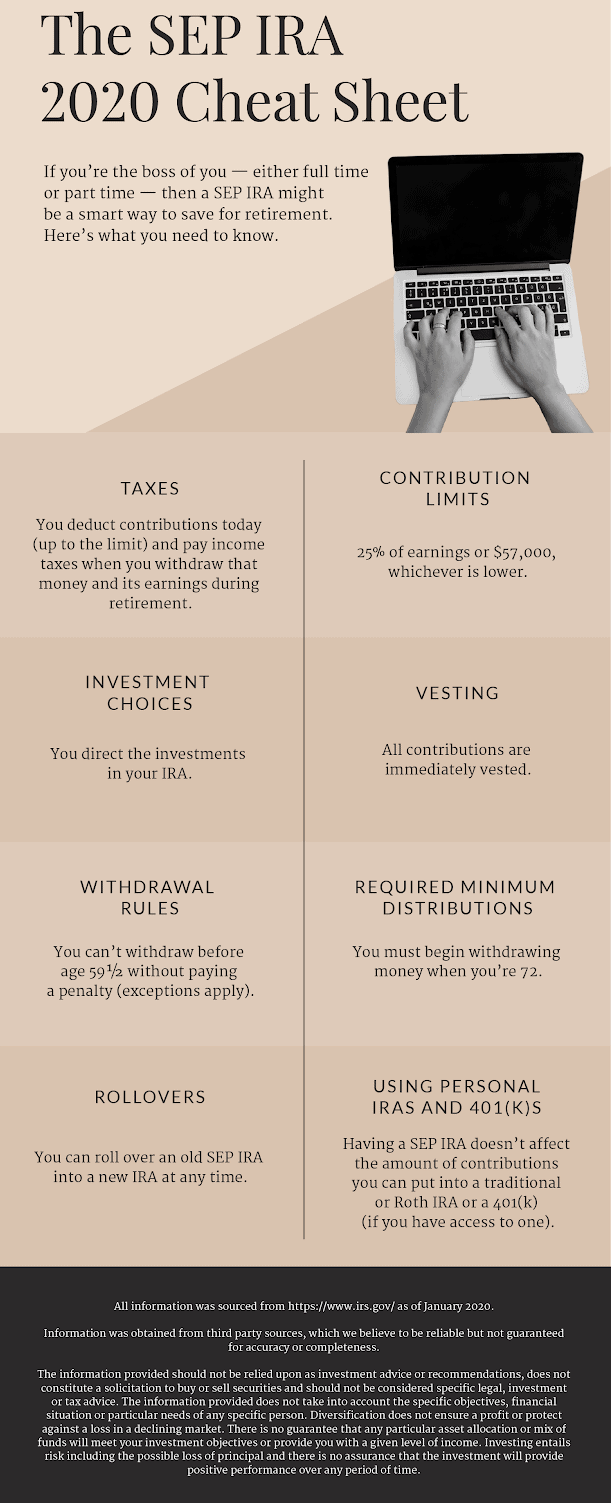

SEP (SIMPLIFIED EMPLOYEE PENSION) IRA

Participants benefit from higher maximum contributions to this account over a traditional IRA. Employers can contribute as much as 25% of employee compensation (limited to $57,000) to employees participating accounts.

So what’s the big difference between the SEP and Simple IRA?

The SEP IRA is best suited for self-employed individuals or sole practitioners wanting to save for their own retirement. As the firm adds employees the employer contribution increases and can become expensive. The SIMPLE IRA relies on salary deferral contributions from the employees; the employer is required to contribute far less to the plan.

Important Takeaways to Understand More Differences

-

- These are tax-deferred retirement accounts.

- Standard tax benefits apply to employer contributions, and most of the tax rules for individual accounts are the same as those applied to traditional IRAs.

- These accounts do not require the start-up and operating costs of most employer-sponsored retirement plans.

- Generally, 100% of all employer contributions are tax-deductible to the business.

- These plans can help small and new businesses with retirement savings.

- Contributions to these plans are 100% vested, and employees make their own investment decisions.

- Except for “Contribution Limit,” the following cheat sheet applies to SIMPLE IRAs as well.

We would love to talk with you about your financial aspirations and needs and how one of these plans might suit your needs. At Muhlenkamp making your money grow is our top priority.

The opinions expressed are those of Muhlenkamp and Company and are not intended to be a forecast of future events, a guarantee of future results, nor investment advice.